Regulate or tax: how to guarantee banking stability?

04/22/2024

6 min

Share

This is THE headache facing financial regulators. How do you prevent banks from taking on too much risk, without discouraging them from lending?

A year ago, the international financial system was in turmoil. In March 2023, four US regional banks, including Silicon Valley Bank, went bankrupt. One of the causes put forward was a relaxation of the rules for medium-sized institutions, with the aim of easing the constraints they faced. Soon after their implementation, the solutions conceived by regulators to reinforce the solidity of American banks are already being criticized.

Questions are being raised about their effectiveness, and in particular about the ever-increasing requirement for banking institutions to hold capital. Is this the only way to regulate bank activity without hindering their contribution to economic growth?

Our work explores the use of other tools.

Capital, a guarantee of stability

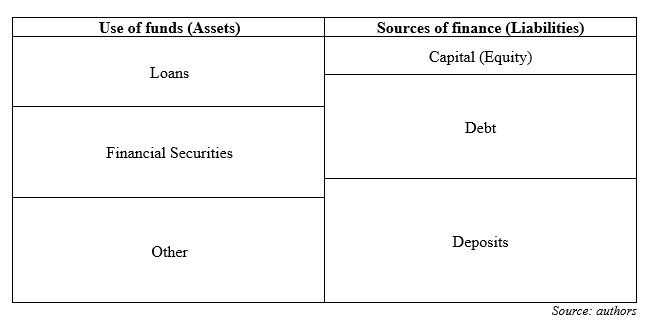

If we were to simplify a bank’s balance sheet, it might look something like this:

On the assets side of the balance sheet are the various activities in which the bank invests. It may choose to grant loans to individuals or companies, and to invest in the financial markets through the purchase and sale of financial securities such as shares and bonds.

To finance its investments, a bank can use a variety of solutions.

On the liabilities side of the balance sheet are the bank’s three main sources of financing: capital, debt and deposits (from individuals and businesses). While capital represents the equity belonging to the bank (reinvested profits from previous years) and its owners/shareholders, debt and deposits are funds lent by other investors, which the bank must repay according to a (more or less fixed) schedule. In the case of debt, these are mainly the bank’s loans and bonds, which must be repaid according to a predetermined schedule and conditions. Deposits, on the other hand, are funds saved by individuals and companies in the institution. In some cases, such as demand deposits (current accounts) and certain savings accounts, repayment can be demanded at any time. This is what happens, for example, when you pay by credit card or withdraw cash.

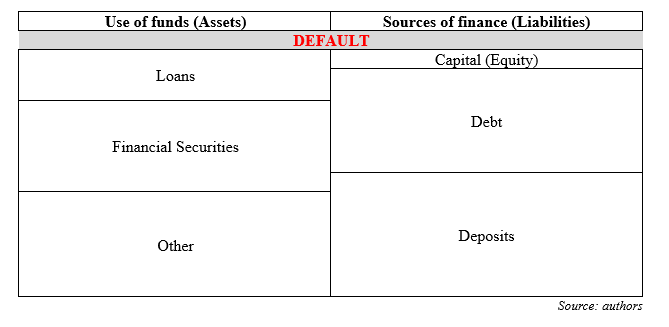

Since it involves no repayment, capital is the most stable source of financing over time. This characteristic also enables a bank to absorb a shock such as the non-repayment of a loan (default) on a credit granted by the bank to a company, for example. If we go back to our diagram above and simulate a default on a loan on the assets side, the total value of the balance sheet will fall, so that total assets will fall by the amount of the loan not repaid, and the shock will be absorbed on the liabilities side by a fall in capital.

If the number of defaults increases by a certain proportion, then capital will not be able to absorb all the losses, causing the bank itself to default on its own debt. In the most extreme case, the institution could be liquidated, leading to a general loss of confidence in the banking sector and contagion to other institutions, which could disrupt the overall functioning of the economy.

This illustration shows the importance of capital as a stabilizing tool for banks. It enables them to fully play their role as financiers of the economy, by being there to invest in individual and business projects. It absorbs a large proportion of the underlying risks, and thus contributes to a country’s economic development. It would therefore be tempting to regulate to encourage banks to make greater use of capital to finance their activities.

Regulating capital: a necessity?

If banks are to be able to manage the risks they take on when granting credit (loans) autonomously, they need to be encouraged to draw on their own financial resources – capital – without having to resort either to debt or to the intervention of a third party (central bank, government) in the event of borrower default. So, what is the minimum level of capital a bank must maintain in relation to the risk of its loans?

In 1988, the Basel Committee introduced the Cooke ratio, calculated as the ratio between the bank’s level of capital and its level of risk-adjusted assets. A minimum threshold of 8% capital is set for all credit institutions (Basel I Accords). In 2004, with the McDonough ratio, the threshold remained at 8%, but the calculation was refined, separating out different types of risk (Basel II Accords). The aim was to encourage banks to be more vigilant and transparent about the nature of their risk exposure.

The collapse of Lehman Brothers and the financial crisis of 2008 marked a turning point. They contributed to the development of the Basel III accords. A new regulatory framework was put in place, with the implementation of new requirements: banks were obliged to further increase their levels of so-called core capital, specifically retained earnings and common shares. In addition, the new regulatory framework extends risk coverage and further restricts leverage, i.e. the use of debt to finance bank activities.

The two major innovations of Basel III are the introduction of two liquidity ratios, encouraging banks to hold more liquidity to better cope with demand, and the fact that capital requirements vary over time. The idea is to smooth credit supply cycles by lending less during phases of economic expansion, in order to maintain a certain level of provisions that can be used during phases of recession.

Faced with these regulatory requirements, banks have two options: increase their capital levels or reduce their exposure to risk by lending less or favoring less risky projects. While the first option seems to be the target of regulators, under certain conditions, asset-level adjustment may be preferred by banks because it is easier to implement, to the detriment of economic growth.

One study has shown that, under Basel II, a 1% increase in capital requirements contributed to a 4.5% reduction in lending. So, what would be the best solution to guarantee the stability of the banking system without hampering economic development? In other words, how can we encourage banks to hold more capital while maintaining their lending activity?

An alternative: taxing debt

An alternative to capital regulation developed in some European countries is to lower the relative cost of equity versus debt, by taxing debt on banks’ balance sheets. As a general rule, borrowing funds through debt is less costly than increasing equity: lenders (debt holders) demand a lower return than shareholders (equity holders), because the risks are not the same. In the event of liquidation, for example, the former will receive their due in priority to the latter.

Against this backdrop, in 2010 the IMF suggested introducing a tax on bank debt in addition to regulatory capital requirements. The aim is to encourage banks to reduce their debt levels, which have become more costly, and thus, indirectly, to find other sources of financing, including capital.

One study points to the success of this initiative in rebalancing bank balance sheets in favor of capital; our work shows that taxing bank debt also helps to support the economy through a higher volume of credit granted.

Not only does an increase in debt taxation lead to a decrease in leverage in favor of an increase in capital, but it also enables the bank to broaden its scope of action and support its credit offer, while complying with the regulatory requirements set by the Basel Committee. It would therefore seem that a combination of regulation and taxation would be the most effective way of maintaining a stable banking system and financial support for the real economy.

Article:

Aurore Burietz, LEM-CNRS 9221, IÉSEG School of Management; Matthieu Picault, Université d’Orléans and Steven Ongena, University of Zurich.

This is a translated version of an article published on The Conversation France. Read the original article in French.

Contributor

Discover more Insights

Economics & Finance

Has the expansion of higher education created regional inequalities? Lessons from Italy …

25/05/2026

7 min

CSR, Sustainability & Diversity

Climate pledges: How EU citizens & experts see these differently (and why this matters)

12/05/2026

4 min

Economics & Finance

Is silver more valuable than gold?

31/03/2026

5 min

Economics & Finance

What defines a liveable city in 2026?

24/02/2026

4 min